Talbot Financial – 1Q 2020 Review

Please find attached your Talbot Financial first quarter 2020 portfolio review to supplement your monthly account statements available from Schwab. The report provides a performance summary of your investment portfolio compared to the S&P 500 Total Return Index (“Index”), Talbot Financial’s benchmark, and lists your investment portfolio holdings by industry sector.

Investment Review

In mid-January, we sent a quarterly update that described a continued robust economy, an accommodative U.S. Federal Reserve policy and an improving tariff environment. Then, the world changed from a global pandemic that has resulted in tragic loss, widespread suffering and will lead to an economic recession.

Specific to the financial markets throughout the quarter, we experienced record level stock price volatility, a 60% drop in crude oil prices and 10-year U.S. Treasury Bond yields that declined to 0.7%. Investors’ nerves were tested, with the Index dropping 33% over the course of five-weeks, only to subsequently rebound 20% in three-days. For the first quarter of 2020, the Index declined almost 20%. In fact, it was the worst quarter for the Index since the 2008 financial crisis. Fortunately, while the financial market moves mentioned above were unprecedented, so too were the monetary and fiscal responses by the government. In both the U.S. and abroad, governments reacted quickly and decisively to mitigate the near-term economic effects of the crisis. Regarding monetary policy, the U.S. Federal Reserve immediately lowered interest rates, increased its Treasury bond buying program and began purchasing corporate debt. Furthermore, swift policy action was taken to provide capital to both individuals and businesses. The U.S. fiscal response currently consists of over $2 trillion of financial stimulus, including enhanced unemployment benefits, cash payments to individuals, providing loans to small businesses and delayed federal tax filings. These programs have generally been viewed as offering much needed beneficial relief to small businesses, consumers and the overall economy. Importantly, fiscal policymakers are also suggesting additional stimulus programs will likely be initiated.

Investment Outlook

Although times are significantly different, our investment strategy remains the same. Talbot Financial managed investment portfolios are constructed with an intent of protecting downside risk, as compared to the broader stock market.

First, we focus on only the highest quality companies with industry leading balance sheets and strong cash flows. In times of stress, the strength of these balance sheets and cash flows provide ballast and the ability for these companies to withstand an economic recession.

Second, the vast majority of the equity holdings in the investment portfolio pay quarterly dividends. Although, we acknowledge dividends may be reduced or suspended in some companies within the portfolio. The current dividend yield on the typical client portfolio is now over 2%, approximately three times greater than the yield on a 10-Year U.S. Treasury-Bond.

Furthermore, we actively manage your investment portfolio. For example, over the past few months we sold shares of companies in your portfolio we felt were most susceptible to an economic downturn and purchased shares in companies we view as being more financially stable with more favorable long-term secular growth opportunities.

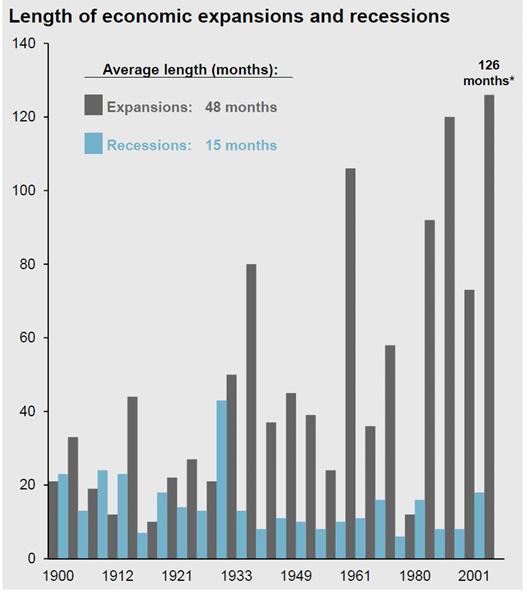

History has demonstrated it is “time in the market”, not “timing the market” that matters. Data from the National Bureau of Economic Research in the following chart shows the length of economic expansions and recessions since 1900. Over this 120-year period, the length of the average recession was 15-months, while the average expansion lasted four-years. More recent data shows that recessions have shortened while expansions have lengthened.

In summary, staying invested in the equity market is how financial wealth is created over time. However, it is essential to plan accordingly to have adequate liquid financial resources available (i.e., cash) in order to avoid selling stocks during the periods of economic recessions.

In late February, as the financial markets were reacting to the evolution of the Coronavirus into a global pandemic, we sent the following as part of an update message:

“Our driving principle is the companies we own in our investment portfolio will be worth more in the future than they are currently worth because of their ability to grow and profit within their respective industries. We believe our focus on investing in well-diversified large companies with solid balance sheets, strong free cash flows and industry leading products and services will be beneficial in the long run. In fact, we feel our value-oriented investment philosophy is better positioned than other types of higher risk investment strategies during times of potential increased market turbulence. Furthermore, it is often during these uncertain times we find opportunities to invest in strong and sustainable companies at discounted prices.” Now almost six-weeks later, our view remains the same.

As always, we welcome the opportunity to review your portfolio in detail. Please do not hesitate to call us with any questions.

Stay healthy!

Talbot Financial, LLC

www.talbotfinancial.com